Platform

Self Service

Subscribers get access to our numerous Tableau dashboards covering healthcare data needed to make investments and better understand the market. We are built for professionals needing a broad range of information in an easy to use format. Typically you can be “up and running” in a few hours either on your own or with an introductory demo session.

vALUE aDD

Every subscription comes with pre-packaged consulting support hours. Healthcare data can be hard to understand. Sometimes a different slice is needed to best fit your business case. Being able to ask a few questions and understand the job to be done makes all the difference. We have refresh and quality check jobs that run from weekly to annual, saving you time and expense and incorporating our expertise.

Information Sets

We are constantly expanding our library. We integrate across healthcare information for quality, experience, census, demographic, actuarial, health plan, macroeconomic, consumer retail, digital, and other valuable information that describe a competitive landscape. We maintain non-public rankings and data partnerships. We can also build in your own data set securely in our data warehouse and accessible only to you. See below.

Technology

The platform is built on HIPAA-compliant Amazon Web Services, Tableau, and other enterprise tools for design/build efficiency, security and on-demand performance. Tableau works on mobile and tablets. However, your preferred tools can connect to the data lake directly, or have data syndicated into your environment. Please ask about our custom “heavy lift” projects working with your team and/or third-parties.

The following sample cases are live at Tableau Public and use publicly available data sets which typically take months to prep, clean, organize and link, and then design/build into reports and dashboards, and finally, integrate our firm’s services know-how. They are provided here “as is” for a quick understanding of some of our capabilities and how/where healthcare professionals could be using analytics more effectively. Contact us to learn more.

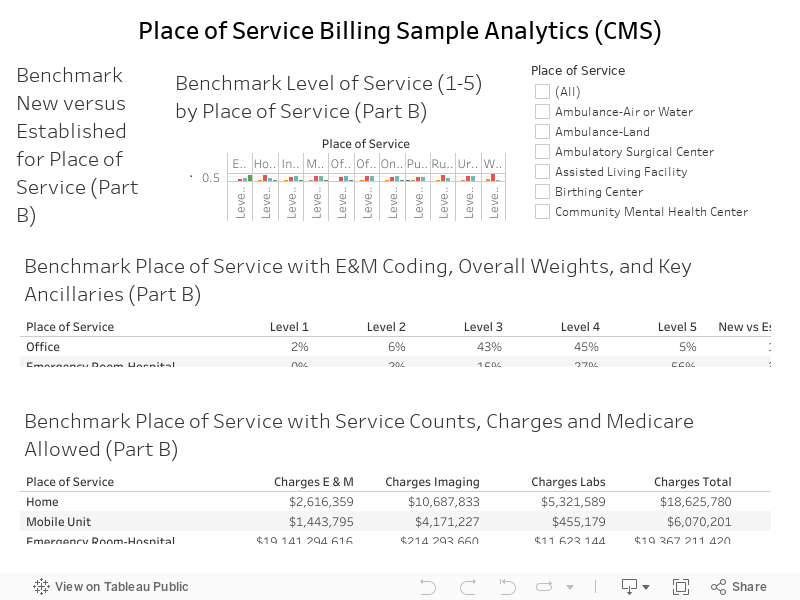

Case 01: Same/similar care, very different settings and price points

The following case study is a quick look at national Medicare coding and key differences across “place of service”. This is typically one of the quickest and most important details in running provider operations. Interesting to note… there are very few actual “retail clinic” locations as filed by place of service, and pretty much everything runs as a physician office. Not shown include things like provider-level performance, taxonomy, registration details that are skewing your commercial plan directory, your market share, and numerous other factors.

We have an appetite for data and analytics

Big picture

The “big picture” starts with the Macroeconomic and Census data with Block-level 1 and 5 Year ACS from US Census; Housing Permits by County; Employment Statistics by County; 10 Year Treasury Rates (hospitals are like banks, depending on how you look at it); Population Growth Forecasts.

Consumerism and ratings

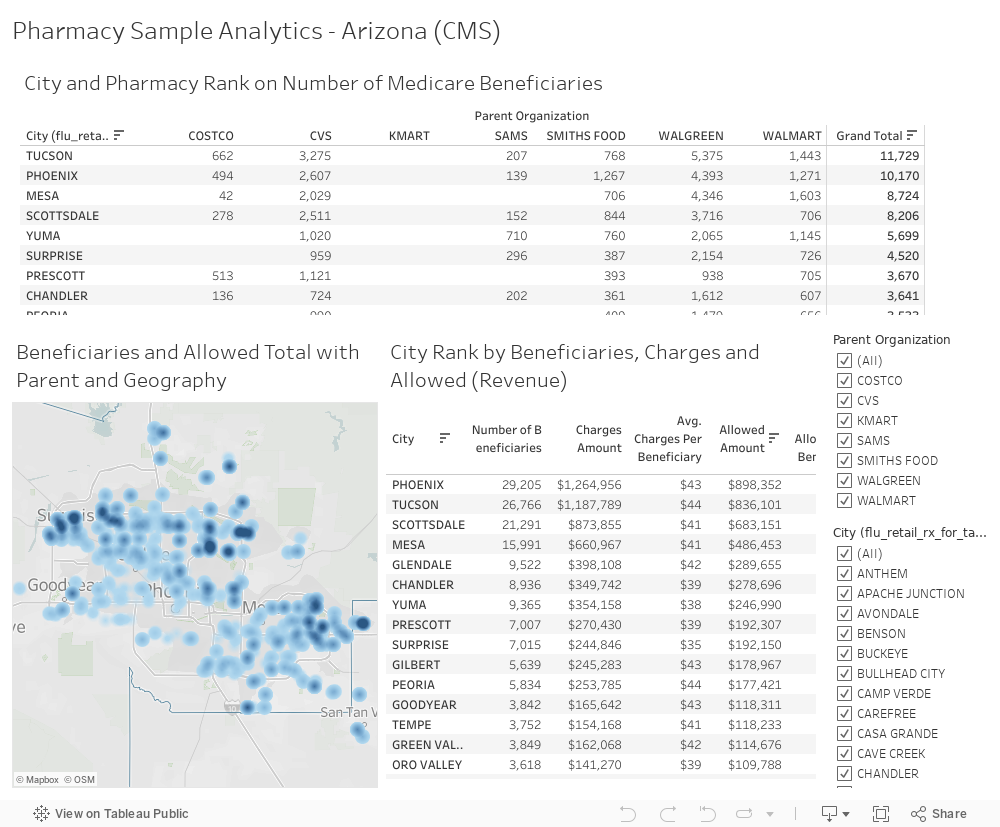

Consumer data include privately sourced Pharmacies and competitors (Walmart, CVS, Walgreens, Target, etc.); Telehealth operators by health plan, health system, and direct-to-consumer; Urgent Care and other chain-type operators sourced from CMS datasets; for hospitals we track quarterly HCAHPS (Hospital Consumer Assessment of Healthcare Providers and Systems).

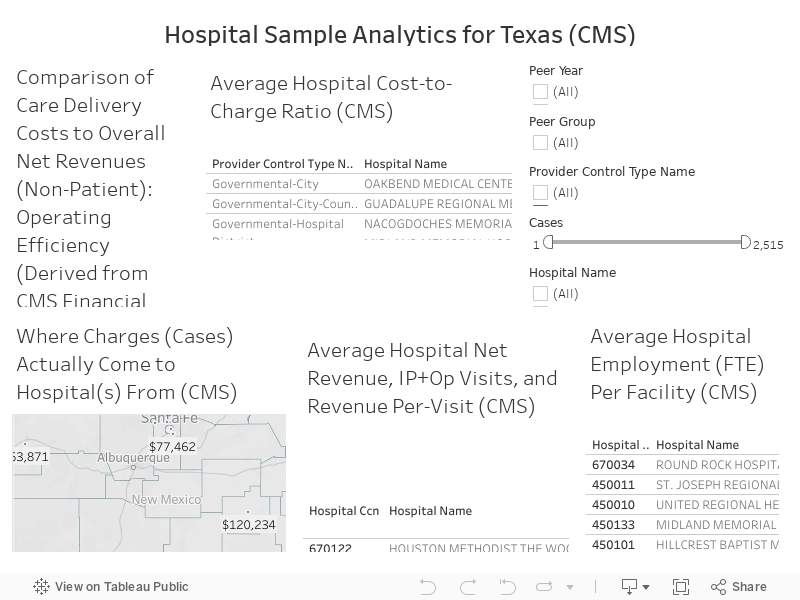

Providers and facilities

We have data for CMS licensed Hospitals (In- and Out-Patient), Doctors and Clinicians, Suppliers, Ambulatory Surgery Centers (ASCs), Nursing Homes, Inpatient Rehabilitation (IRFs), Skilled Nursing (SNFs), Home Health, Renal (Dialysis), Hospice, and state-level sources. We include the Hospital service area data and Place of Service (POS), and Provider / CPT Utilization metrics.

Quality

Numerous measures at the facility level describe quality at hospitals such as emergency department wait times and throughput, timely and effective care, complications, readmissions and deaths, use of medical imaging, payment and value of care, along with national and state benchmarks. We also have Hospital Value-Based Purchasing (HVBP) quality incentive program data.

Financial and Utilization data (10+ Years)

Reimbursement data (Cost Reports) on hospitals and other licensed facilities provide a wealth of insight going back a decade on key statistics like bed utilization and productivity, number of employees, ownership, compensation, income and balance sheet financials, uncompensated care, cost to charge ratios, and much more. A literal goldmine at the hospital and other licensed facility level.

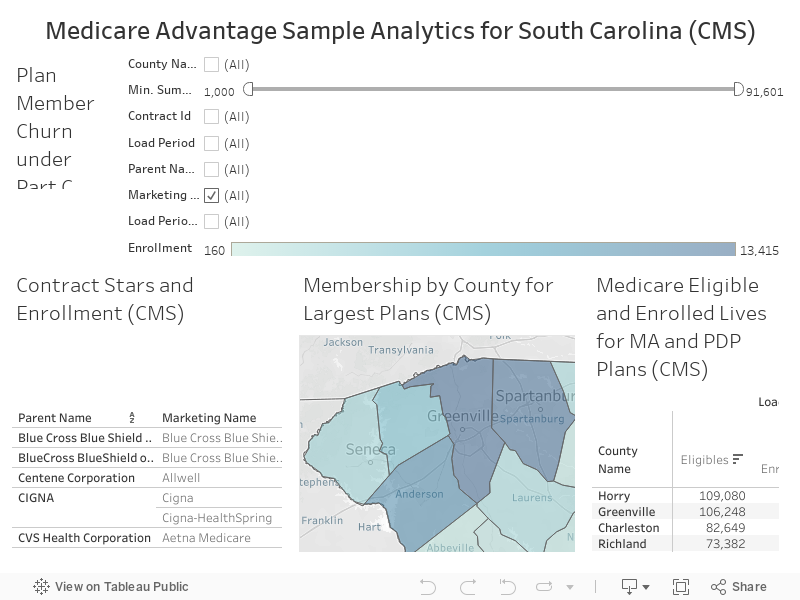

Traditional Medicare & Medicare Advantage

Traditional Medicare and Medicare Advantage data include various measures and spending for both since 2007 to 2018. Contract/plan, penetration, and enrollment data are captured at a county-level each month for both eligible and enrolled. Star Ratings and plan-level benefit package describing premium/MOOP/all features are per year (as of most recent). This includes detailed SNP, MA, MA-PDP, and PDP with plan directory and low income subsidy data.

Demand-side Measures

We round out our analytics with actuarially stable incidence data to derive demand curves, for example incidence of renal disease requiring dialysis per capita, number of ear aches driving office visits, etc. These tend to be diagnosis or condition driven, and these are used to forecast (tied to population factors) many common ambulatory and facility-based services. Functionally these derive the “demand curve” in a given market.

claims and state-level measures

Claims (Public) Medicare Provider Utilization and Payment Data (MEDPAR) summarizes the utilization and payments for procedures, services, and drugs provided to Medicare beneficiaries by inpatient and outpatient hospitals, physicians, and other suppliers. Claims (Non-Public) for providers, in- and outpatient encounters at the beneficiary claim detail (January 2021). State-level data varies.